Exhibit 99.1

November 2018

Forward Looking Statements 1 all data as of 09/30/2018 unless otherwise stated This presentation is for informational purposes only and does not constitute an offer to sell, or a solicitation of offers to purchase, Global Medical REIT Inc . ’s (the “Company”, or “GMRE”) securities . The information contained in this presentation does not purport to be complete and should not be relied upon as a basis for making an investment decision in the Company’s securities . This presentation also contains statements that, to the extent they are not recitations of historical fact, constitute “forward - looking statements . ” Forward - looking statements are typically identified by the use of terms such as “may,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology . The forward - looking statements included herein are based upon the Company’s current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties . Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the Company’s control . Although the Company believes that the expectations reflected in such forward - looking statements are based on reasonable assumptions, the Company’s actual results and performance could differ materially from those set forth in the forward - looking statements due to the impact of many factors including, but not limited to, those discussed under “Risk Factors” in the Company’s Annual Report on Form 10 - K and Quarterly Reports on Form 10 - Q and any prospectus or prospectus supplement filed with the Securities and Exchange Commission . The Company undertakes no obligation to update or revise any such information for any reason after the date of this presentation, unless required by law . This presentation includes information regarding certain of our tenants, which are not subject to SEC reporting requirements . The information related to our tenants contained in this report was provided to us by such tenants or was derived from publicly available information . We have not independently investigated or verified this information . We have no reason to believe that this information is inaccurate in any material respect, but we cannot provide any assurance of its accuracy . We are providing this data for informational purposes only .

ABOUT GMRE

GMRE Value Proposition Net lease operating platform, which tends to be more resilient during economic fluctuations Healthcare facilities providing mission critical services with leading operators Proven investment strategy Resulting in Operational Flexibility for Tenants and Improved Asset Value D IFFERENTIATED S TRATEGY Primary focus on physician and real estate tenants with triple - net lease structures Meticulous underwriting with multiple layers of review and approvals for acquisitions Investments are structured with favorable credit support and attractive lease coverage ratios Long - term demographic tailwinds – increasing specialization and localization of healthcare delivery Robust investment pipeline driven by a strong network that facilitates referral - based transactions with attractive pricing Deep market of high - quality assets with attractive cap rates in non - gateway markets Management team with extensive expertise in healthcare real estate acquisitions, finance, development and administration Average over 20 years of experience with deep relationships in the space D ISCIPLINED EXECUTION L ARGE M ARKET O PPORTUNITY S EASONED M ANAGEMENT T EAM 3 all data as of 09/30/2018 unless otherwise stated

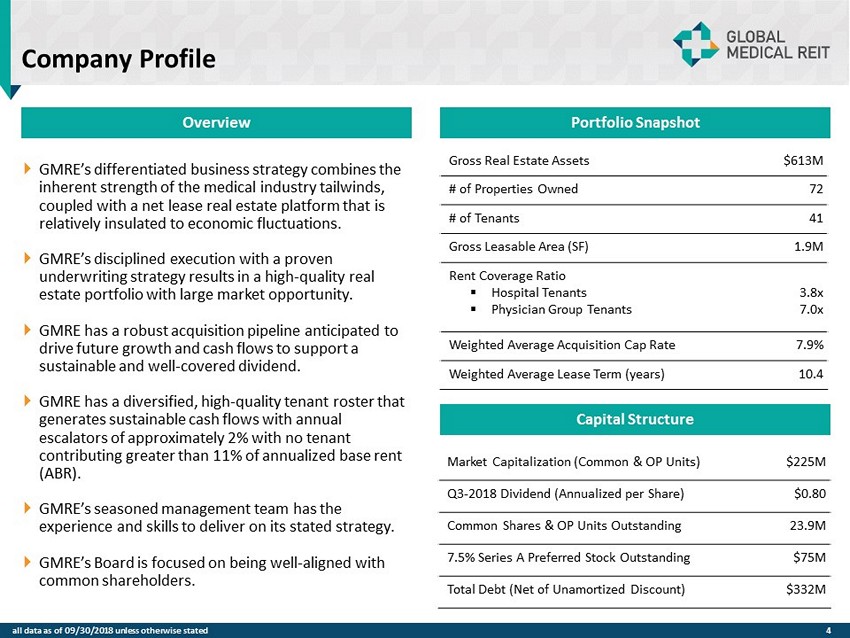

Overview GMRE’s differentiated business strategy combines the inherent strength of the medical industry tailwinds, coupled with a net lease real estate platform that is relatively insulated to economic fluctuations. GMRE’s disciplined execution with a proven underwriting strategy results in a high - quality real estate portfolio with large market opportunity. GMRE has a robust acquisition pipeline anticipated to drive future growth and cash flows to support a sustainable and well - covered dividend. GMRE has a diversified, high - quality tenant roster that generates sustainable cash flows with annual escalators of approximately 2% with no tenant contributing greater than 11% of annualized base rent (ABR). GMRE’s seasoned management team has the experience and skills to deliver on its stated strategy. GMRE’s Board is focused on being well - aligned with common shareholders. Company Profile Portfolio Snapshot Gross Real Estate Assets $613M # of Properties Owned 72 # of Tenants 41 Gross Leasable Area (SF) 1.9M Rent Coverage Ratio ▪ Hospital Tenants ▪ Physician Group Tenants 3.8x 7.0x Weighted Average Acquisition Cap Rate 7.9% Weighted Average Lease Term (years) 10.4 Market Capitalization (Common & OP Units) $225M Q3 - 2018 Dividend (Annualized per Share) $0.80 Common Shares & OP Units Outstanding 23.9M 7.5% Series A Preferred Stock Outstanding $75M Total Debt (Net of Unamortized Discount) $332M Portfolio Snapshot Capital Structure 4 all data as of 09/30/2018 unless otherwise stated

GMRE STRATEGY

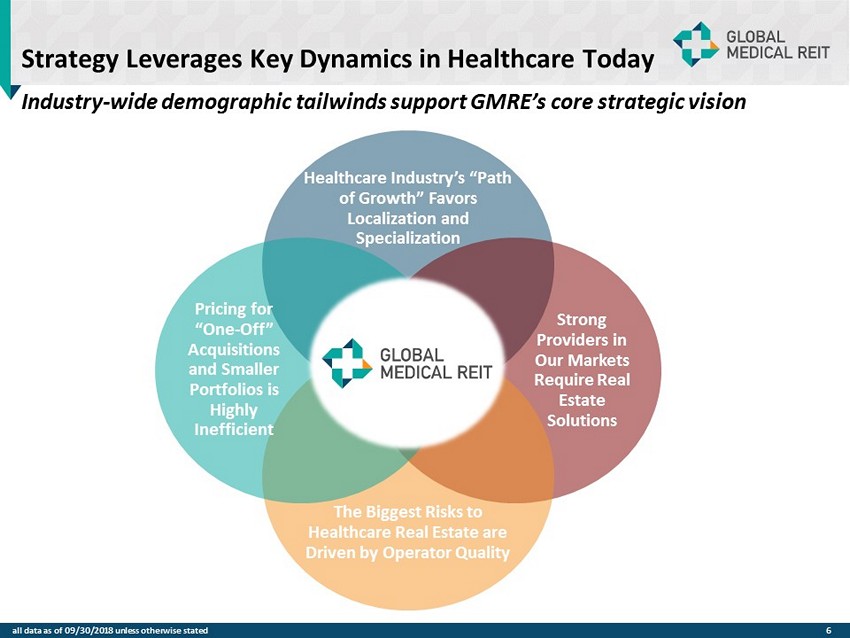

Strategy Leverages Key Dynamics in Healthcare Today Industry - wide demographic tailwinds support GMRE’s core strategic vision Healthcare Industry’s “Path of Growth” Favors Localization and Specialization Strong Providers in Our Markets Require Real Estate Solutions The Biggest Risks to Healthcare Real Estate are Driven by Operator Quality Pricing for “One - Off” Acquisitions and Smaller Portfolios is Highly Inefficient 6 all data as of 09/30/2018 unless otherwise stated

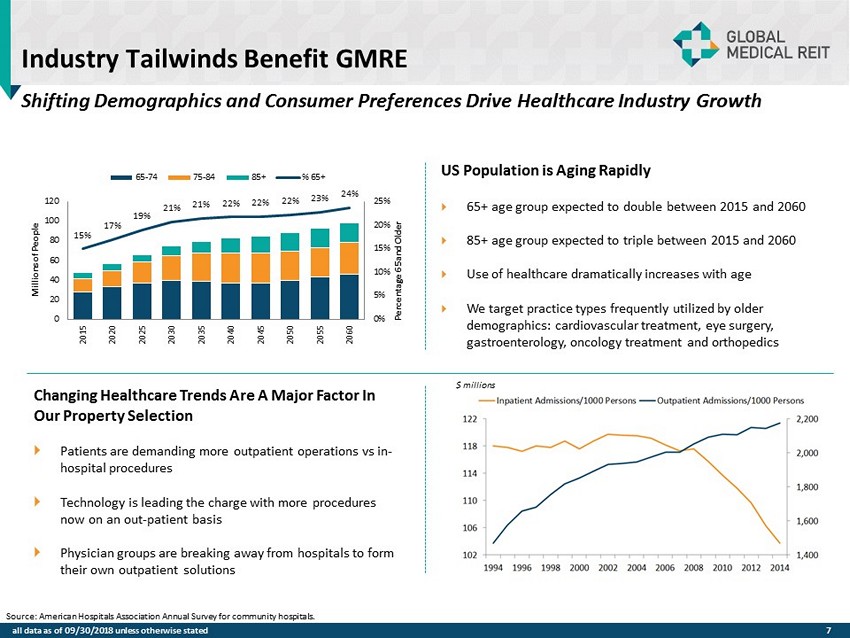

Shifting Demographics and Consumer Preferences Drive Healthcare Industry Growth Industry Tailwinds Benefit GMRE US Population is Aging Rapidly 65+ age group expected to double between 2015 and 2060 85+ age group expected to triple between 2015 and 2060 Use of healthcare dramatically increases with age We target practice types frequently utilized by older demographics: cardiovascular treatment, eye surgery, gastroenterology, oncology treatment and orthopedics Changing Healthcare Trends Are A Major Factor In Our Property Selection Patients are demanding more outpatient operations vs in - hospital procedures Technology is leading the charge with more procedures now on an out - patient basis Physician groups are breaking away from hospitals to form their own outpatient solutions 15% 17% 19% 21% 21% 22% 22% 22% 23% 24% 0% 5% 10% 15% 20% 25% 0 20 40 60 80 100 120 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 Percentage 65 and Older Millions of People 65-74 75-84 85+ % 65+ Source: American Hospitals Association Annual Survey for community hospitals. $ millions 7 all data as of 09/30/2018 unless otherwise stated

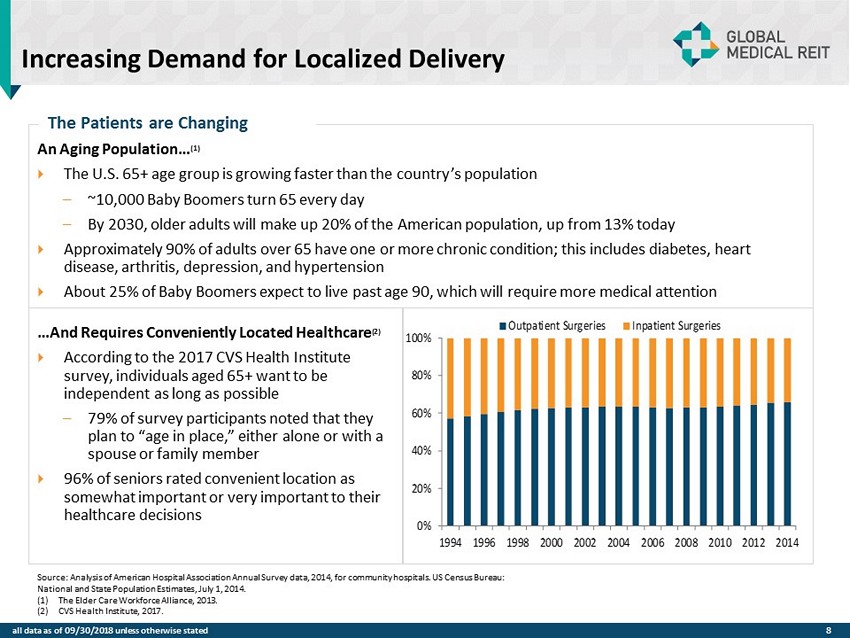

Increasing Demand for Localized Delivery 0% 20% 40% 60% 80% 100% 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 Outpatient Surgeries Inpatient Surgeries An Aging Population… (1) The U.S. 65+ age group is growing faster than the country’s population – ~10,000 Baby Boomers turn 65 every day – By 2030, older adults will make up 20% of the American population, up from 13% today Approximately 90% of adults over 65 have one or more chronic condition; this includes diabetes, heart disease, arthritis, depression, and hypertension About 25% of Baby Boomers expect to live past age 90, which will require more medical attention The Patients are Changing Source: Analysis of American Hospital Association Annual Survey data, 2014, for community hospitals. US Census Bureau: National and State Population Estimates, July 1, 2014. (1) The Elder Care Workforce Alliance, 2013. (2) CVS Health Institute, 2017. …And Requires Conveniently Located Healthcare (2) According to the 2017 CVS Health Institute survey, individuals aged 65+ want to be independent as long as possible – 79% of survey participants noted that they plan to “age in place,” either alone or with a spouse or family member 96% of seniors rated convenient location as somewhat important or very important to their healthcare decisions 8 all data as of 09/30/2018 unless otherwise stated

Disciplined Yet Opportunistic Acquisition Strategy We aim to create a property portfolio comprised substantially of off - campus, purpose - built, licensed medical facilities such as MOBs, specialty hospitals, IRFs and ASCs, that are geographically situated to take advantage of the aging U.S. population and the decentralization of healthcare TENANTS MARKETS / LOCATIONS FACILITIES x Strong providers with leading market share x Rent guarantees and other credit protection x Specialization in age - related procedures x Operators with regional footprints x Strong and diversified payor mix and history x Institutional quality x Purpose - built real estate x Single tenant focus with selective multi - tenant acquisitions x Class A / Recent construction or renovation x Amenitized patient areas x Convenient access / location x Long - term leases with annual rent escalations x Healthcare market with clear and quantifiable competitive dynamics x Positioned to benefit from ongoing decentralization trends in healthcare x Proximity to related resources x Long - term positive demand drivers (population growth and demographics) x Barriers to competition 9 all data as of 09/30/2018 unless otherwise stated

Future Growth Strategies GMRE consistently maintains a large pipeline of actionable acquisition opportunities to sustain growth as a result of being an attractive deal partner Flexible Partner Ability to navigate complex situations via an adaptable approach to negotiations and deal structuring has created a favorable reputation in the market Strong Broker Relationships Reach via a broad network of investment sales brokers have driven direct referrals to prospective sellers Certainty of Closing Lack of dependence on debt financing to pursue transactions minimizes conditionality of bids Use of OP Units Use of OP Units provides efficient use of equity currency while providing sellers with an attractive, tax - advantage form of consideration and providing us with attractive pricing as evidenced in 3 transactions completed since 2017 10 all data as of 09/30/2018 unless otherwise stated

GMRE PORTFOLIO

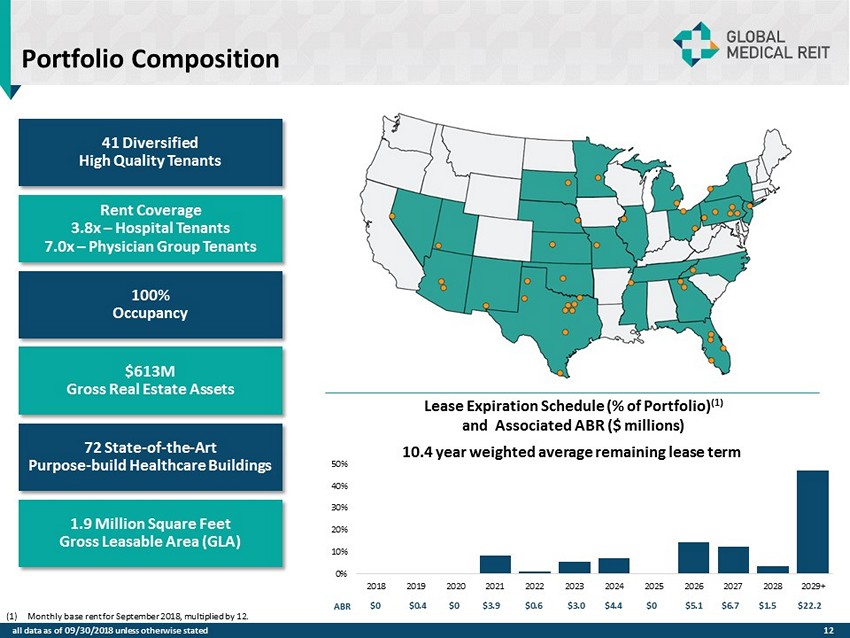

Portfolio Composition (1) Monthly base rent for September 2018, multiplied by 12. $ 613M Gross Real Estate Assets 72 State - of - the - Art Purpose - build Healthcare Buildings Rent Coverage 3.8x – Hospital Tenants 7.0x – Physician Group Tenants 100% Occupancy 1.9 Million Square Feet Gross Leasable Area (GLA) 41 Diversified High Quality Tenants Lease Expiration Schedule (% of Portfolio) (1) and Associated ABR ($ millions) 10.4 year weighted average remaining lease term 12 all data as of 09/30/2018 unless otherwise stated 0% 10% 20% 30% 40% 50% 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029+ $0 $0.4 $0 $3.9 $0.6 $3.0 $4.4 $0 $5.1 $6.7 $1.5 $22.2 ABR

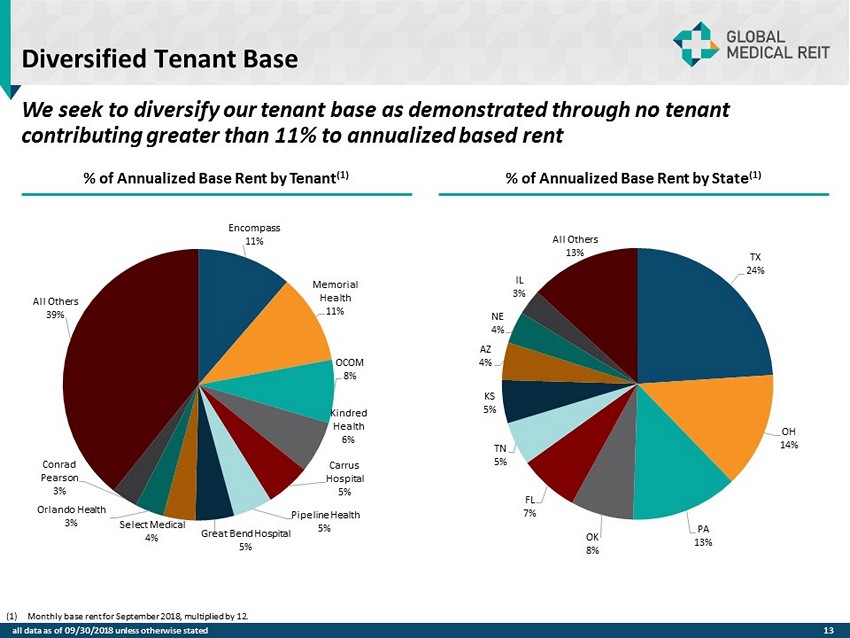

Diversified Tenant Base (1) Monthly base rent for September 2018, multiplied by 12. % of Annualized Base Rent by State (1) % of Annualized Base Rent by Tenant (1) We seek to diversify our tenant base as demonstrated through no tenant contributing greater than 11% to annualized based rent 13 all data as of 09/30/2018 unless otherwise stated Encompass 11% Memorial Health 11% OCOM 8% Kindred Health 6% Carrus Hospital 5% Pipeline Health 5% Great Bend Hospital 5% Select Medical 4% Orlando Health 3% Conrad Pearson 3% All Others 39% TX 24% OH 14% PA 13% OK 8% FL 7% TN 5% KS 5% AZ 4% NE 4% IL 3% All Others 13%

Established Strong Healthcare Operators Not - For - Profit Health System Affiliations For - Profit Systems Affiliations and Surgical Operator Partnerships Dominant Local Physician Groups 14 all data as of 09/30/2018 unless otherwise stated

GMRE CASE STUDIES

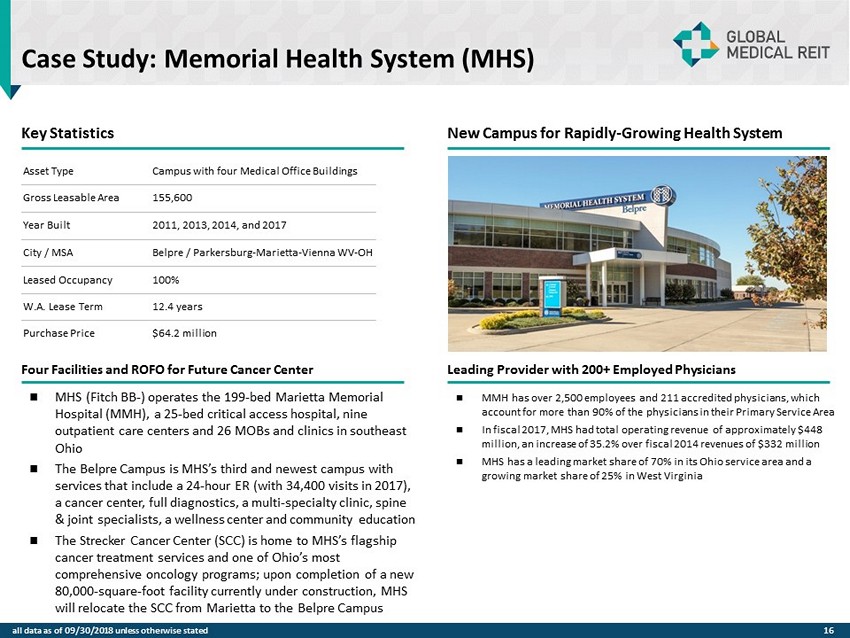

Case Study: Memorial Health System (MHS) Key Statistics New Campus for Rapidly - Growing Health System Four Facilities and ROFO for Future Cancer Center Leading Provider with 200+ Employed Physicians MHS (Fitch BB - ) operates the 199 - bed Marietta Memorial Hospital (MMH), a 25 - bed critical access hospital, nine outpatient care centers and 26 MOBs and clinics in southeast Ohio The Belpre Campus is MHS’s third and newest campus with services that include a 24 - hour ER (with 34,400 visits in 2017), a cancer center, full diagnostics, a multi - specialty clinic, spine & joint specialists, a wellness center and community education The Strecker Cancer Center (SCC) is home to MHS’s flagship cancer treatment services and one of Ohio’s most comprehensive oncology programs; upon completion of a new 80,000 - square - foot facility currently under construction, MHS will relocate the SCC from Marietta to the Belpre Campus MMH has over 2,500 employees and 211 accredited physicians, which account for more than 90% of the physicians in their Primary Service Area In fiscal 2017, MHS had total operating revenue of approximately $448 million, an increase of 35.2% over fiscal 2014 revenues of $332 million MHS has a leading market share of 70% in its Ohio service area and a growing market share of 25% in West Virginia Asset Type Campus with four Medical Office Buildings Gross Leasable Area 155 ,600 Year Built 2011, 2013, 2014, and 2017 City / MSA Belpre / Parkersburg - Marietta - Vienna WV - OH Leased Occupancy 100% W.A. Lease Term 1 2 .4 years Purchase Price $ 64 .2 million 16 all data as of 09/30/2018 unless otherwise stated

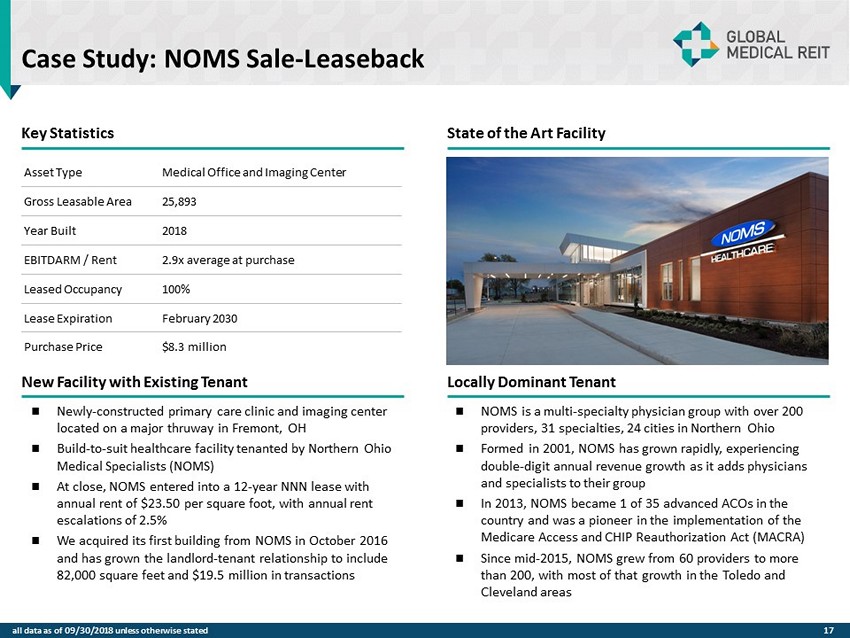

Case Study: NOMS Sale - Leaseback Key Statistics State of the Art Facility New Facility with Existing Tenant Locally Dominant Tenant Asset Type Medical Office and Imaging Center Gross Leasable Area 25,893 2018 EBITDARM / Rent 2.9 x average at purchase Leased Occupancy 100% Lease Expiration February 2030 Purchase Price $8.3 million Year Built Newly - constructed primary care clinic and imaging center located on a major thruway in Fremont, OH Build - to - suit healthcare facility tenanted by Northern Ohio Medical Specialists (NOMS) At close, NOMS entered into a 12 - year NNN lease with annual rent of $23.50 per square foot, with annual rent escalations of 2.5% We acquired its first building from NOMS in October 2016 and has grown the landlord - tenant relationship to include 82,000 square feet and $19.5 million in transactions NOMS is a multi - specialty physician group with over 200 providers, 31 specialties, 24 cities in Northern Ohio Formed in 2001, NOMS has grown rapidly, experiencing double - digit annual revenue growth as it adds physicians and specialists to their group In 2013, NOMS became 1 of 35 advanced ACOs in the country and was a pioneer in the implementation of the Medicare Access and CHIP Reauthorization Act (MACRA) Since mid - 2015, NOMS grew from 60 providers to more than 200, with most of that growth in the Toledo and Cleveland areas 17 all data as of 09/30/2018 unless otherwise stated

APPENDIX

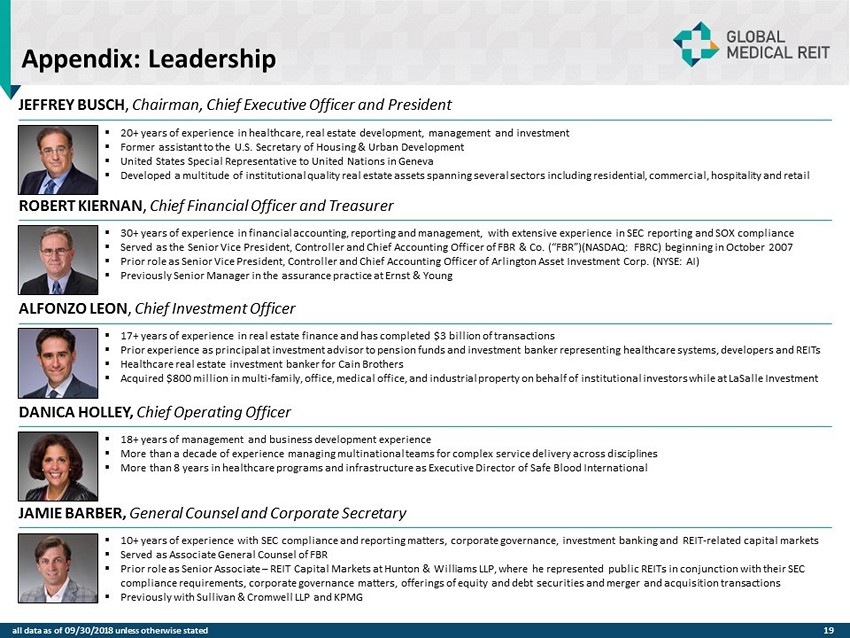

Appendix: Leadership JEFFREY BUSCH , Chairman, Chief Executive Officer and President ROBERT KIERNAN , Chief Financial Officer and Treasurer ALFONZO LEON , Chief Investment Officer ▪ 17 + years of experience in real estate finance and has completed $ 3 billion of transactions ▪ Prior experience as principal at investment advisor to pension funds and investment banker representing healthcare systems, d eve lopers and REITs ▪ Healthcare real estate investment banker for Cain Brothers ▪ Acquired $ 800 million in multi - family, office, medical office, and industrial property on behalf of institutional investors while at LaSalle Investment DANICA HOLLEY, Chief Operating Officer ▪ 18 + years of management and business development experience ▪ More than a decade of experience managing multinational teams for complex service delivery across disciplines ▪ More than 8 years in healthcare programs and infrastructure as Executive Director of Safe Blood International ▪ 10+ years of experience with SEC compliance and reporting matters, corporate governance, investment banking and REIT - related ca pital markets ▪ Served as Associate General Counsel of FBR ▪ Prior role as Senior Associate – REIT Capital Markets at Hunton & Williams LLP, where he represented public REITs in conjunction with their SEC compliance requirements, corporate governance matters, offerings of equity and debt securities and merger and acquisition tra nsa ctions ▪ Previously with Sullivan & Cromwell LLP and KPMG JAMIE BARBER, General Counsel and Corporate Secretary ▪ 20+ years of experience in healthcare, real estate development, management and investment ▪ Former assistant to the U.S. Secretary of Housing & Urban Development ▪ United States Special Representative to United Nations in Geneva ▪ Developed a multitude of institutional quality real estate assets spanning several sectors including residential, commercial, ho spitality and retail ▪ 30+ years of experience in financial accounting, reporting and management, with extensive experience in SEC reporting and SOX co mpliance ▪ Served as the Senior Vice President, Controller and Chief Accounting Officer of FBR & Co. (“FBR”)(NASDAQ: FBRC) beginning in Oct ober 2007 ▪ Prior role as Senior Vice President, Controller and Chief Accounting Officer of Arlington Asset Investment Corp. (NYSE: AI) ▪ Previously Senior Manager in the assurance practice at Ernst & Young 19 all data as of 09/30/2018 unless otherwise stated

Appendix: Independent Directors Majority independent Board with strong backgrounds in healthcare, real estate and capital markets Henry Cole ▪ President of Global Development International, providing development support and oversight for initiatives in medical and hea lth care programs (e.g. Instant Labs Medical Diagnostics, MedPharm & MPRC Group) ▪ Former President and Founder of international programs at The Futures Group International, a healthcare consulting firm ▪ Director of International Health and Population Programs for GE’s Center for Advanced Studies ▪ Yale (B.S.); Johns Hopkins (MA) Matthew Cypher, Ph.D. ▪ Director of the Steers Center for Global Real Estate and Atara Kaufman Professor of Real Estate at Georgetown University’s McDonough School of Business ▪ Former director at Invesco Real Estate (NYSE: IVR) where he was responsible for oversight of the Underwriting Group, which ac qui red $10.2 billion worth of institutional real estate ▪ Underwrote $1.5 billion of acquisitions and oversaw the Valuations group, which marked to market Invesco’s more than $13 bill ion North American portfolio ▪ Penn State University (B.S.); Texas A&M University (M.S. and Ph.D.) Lori Wittman ▪ Served as the Chief Financial Officer for Care Capital Properties, Inc . (NYSE : CCP) (“Care Capital”), a publicly - traded REIT which was originally formed as a spin - off from Ventas, Inc . (NYSE : VTR) (“Ventas”) and owned over 340 healthcare properties nationwide and had an enterprise value of approximately $ 3 . 5 billion prior to its acquisition by Sabra Healthcare in August 2017 ▪ University of Chicago (M . B . A . , Finance & Accounting) ; University of Pennsylvania (M . C . P . , Housing & Real Estate Finance) Clark University (B . A . ) Ronald Marston ▪ Founder and CEO of Health Care Corporation of America (HCCA) Management Company, originally a subsidiary of Hospital Corporation of America (HCA) ▪ 30 + years in international healthcare focused on healthcare systems with prior experience developing the Twelfth Evacuation Hospital in Vietnam ▪ Tennessee Technological University (B . S . ) ; California Western University (Ph . D . ) ▪ Rear Admiral (Retired) and Chief Veterinary Medical Officer of United States Public Health Service ▪ Former Assistant United States Surgeon General, point person for global development support with a focus on less developed countries ▪ Epidemic Intelligence Service Officer with the U . S . Centers for Disease Control and Prevention (CDC) ▪ Chief epidemiologist with the Centers of Devices and Radiological Health in the US Food and Drug Administration (FDA) ▪ Tuskegee University (B . S . & DVM) ; University in Michigan (M . P . H . ) ; Johns Hopkins University (Ph . D . ) Dr. Roscoe Moore Paula Crowley ▪ Current Chair Emeritus of Anchor Health Properties, previously Chairman of the Board from October 2015 through November 2017 ▪ Co - founder and former CEO of Anchor Health Properties which was sold to Brinkman Management and Development in October 2015 ▪ Prior to Anchor, spent eight year as Development Director with The Rouse Company of Columbia, Maryland ▪ University of Pennsylvania (M.B.A., Masters in City Planning); Middlebury College (B.A.) 20 all data as of 09/30/2018 unless otherwise stated

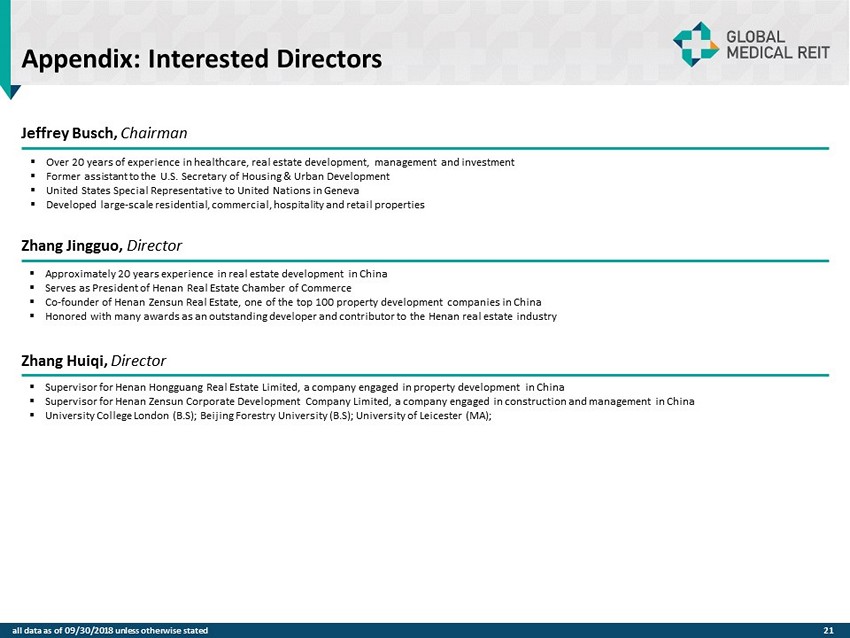

Appendix: Interested Directors Jeffrey Busch, Chairman ▪ Over 20 years of experience in healthcare, real estate development, management and investment ▪ Former assistant to the U.S. Secretary of Housing & Urban Development ▪ United States Special Representative to United Nations in Geneva ▪ Developed large - scale residential, commercial, hospitality and retail properties Zhang Jingguo , Director ▪ Approximately 20 years experience in real estate development in China ▪ Serves as President of Henan Real Estate Chamber of Commerce ▪ Co - founder of Henan Zensun Real Estate, one of the top 100 property development companies in China ▪ Honored with many awards as an outstanding developer and contributor to the Henan real estate industry ▪ Supervisor for Henan Hongguang Real Estate Limited, a company engaged in property development in China ▪ Supervisor for Henan Zensun Corporate Development Company Limited, a company engaged in construction and management in China ▪ University College London (B . S) ; Beijing Forestry University (B . S) ; University of Leicester (MA) ; Zhang Huiqi , Director 21 all data as of 09/30/2018 unless otherwise stated

A Path to Internalized Operations Upon achieving scale, we continue to evaluate internalizing management $500 million of shareholders’ equity is a precursor to internalization Board will appoint a special committee to review the internalization process Two - thirds vote required by our independent directors Internalization may occur with 30 days’ notice Internalization will likely result in a termination fee Termination fee equals the product of 3.0 and the sum of a) base management fee and b) average incentive fee earned over the prior 8 fiscal quarters (no incentive fees have been incurred to - date) straightforward internalization transaction process Allow for both a streamlined evaluation for moving forward as well as transparency for investors $500 Million Shareholder Equity Two - Thirds Vote by Independent Directors Termination Fee Straightforward Process 22 all data as of 09/30/2018 unless otherwise stated

Investor Relations Contact maryj@globalmedicalreit.com (202) 524 - 6869 Thank You